The growing demand for forward-looking information will put a sharper focus on integrated corporate planning. Experience shows that the introduction of effective planning processes is a big challenge in many organizations.

From an investor’s point of view, the anticipation of the future development of a company is of great importance. Companies comply with this requirement by publishing planning data on KPIs that at the same time represent some of the key objectives in internal reporting. Thus corporate planning, previously a rather internal instrument, is also moving into the focus of corporate reporting.

In many companies, planning processes are far from being optimized. Gathering and consolidating accurate planning data consumes a lot of time and resources, whereas the accuracy of planning data quite often proves to be rather poor. The implementation of IT-based planning tools seems not to have brought the improvements that were hoped for. What makes planning processes so difficult to optimize? In our experience, one immanent problem of corporate planning is confusing efficiency with effectiveness.

Effective Planning = Planning the right things

Planning is not a purpose in itself. It has a distinct importance for internal and external stakeholders. The main purpose is to generate a projection of the future development of a company. It is the basis for management decisions, internal target-setting and controlling. It is also the basis to fulfill the growing demand for forward-looking information by external stakeholders.

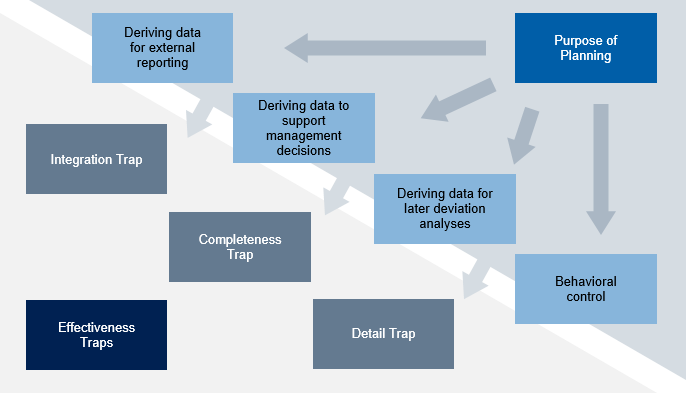

Point of View Paper Effectiveness Traps in Corporate Planning

Planning is only effective if it serves these purposes. On the contrary, planning content that does not serve these purposes is not effective. Thus the identification of the specific purpose of planning has to be the first step in any process re-design. This is a challenging task, as information requirements by internal decision makers and external stakeholders are subjective and dynamic. A clear and stable specification of what data a planning process should deliver is very difficult. At the same time modern planning tools allow almost any requirement possible. This opens what we call “Effectiveness Traps”. They result from the intention to create a process that can fulfill as many potential future requirements as possible. Overlooking them will result in overly complex and inflexible processes:

-

The Completeness Trap

An underlying belief in many planning projects is that a company needs all functions to be included in planning, so that the resulting data is complete and consistent. As understandable as this aim is, it can be the initial cause for an ever growing complexity. For example one could think that planning revenues is not enough but needs to be validated by also planning prices and sales volumes. Not only assets might be planned, but also investments and originating depreciations, so that there are no inconsistencies in the derived data. If this complexity is not yet a problem by itself, it can easily lead into follow-up issues:

-

The Integration Trap

Modern planning systems can enforce integration between planning topics. If investments are planned, depreciations can be calculated and directly synchronized with P&L planning. Planning of headcounts can be integrated with cost and cash flow planning etc. Achieving a high level of integration between a number of functional areas is fascinating but will leverage complexity, because it forces you into ever more detail. For example the direct integration of cost and headcount planning will require headcount planning to include employee categories, salary developments etc. A direct integrating between balance sheet and cash flow planning might require to add the detail of movement types to balance sheet planning in order to correctly distinguish cash relevant from cash irrelevant balance developments.

Integration therefore needs to be defined with care. Maximum direct integration is not necessarily what is required for effective corporate planning and reporting.

-

The Detail Trap

Planning by definition has uncertainty in it. It is a common misunderstanding that more detail automatically means less uncertainty and more accurate planning data. Detailed planning in fact only makes sense if it serves a purpose, e.g. if these detailed data are required for internal decision support or deviation analysis. Otherwise more detail does not add effectiveness, but will even reduce data accuracy. This happens if the operational job of capturing a high number of granular data takes the lead over the anticipation of what future developments will mean for the business and the expected key indicators.

Overcoming traps for better corporate planning – and reporting

A purely technical approach should be avoided when optimizing corporate planning, as this usually puts the focus on efficiency, not so much on the effectiveness of planning. A process is efficient if its output is achieved with the least possible effort. IT can bring fundamental benefits, but even though modern systems are used, the performance of corporate planning will remain poor, if ineffective processes are cemented inside them. As forward-looking data becomes more important for capital market participants, external reporting requirements and the internal creation process has to be considered right from the beginning. Whereas planning was merely considered an internal topic within strategy, finance and business development, the corporate functions of accounting, investor relations communications and sustainability will be more involved in the future. This demands from companies to even more carefully look at their pro- cesses and the traps mentioned here to guarantee effectiveness.

By Andreas Krüger and André Müller